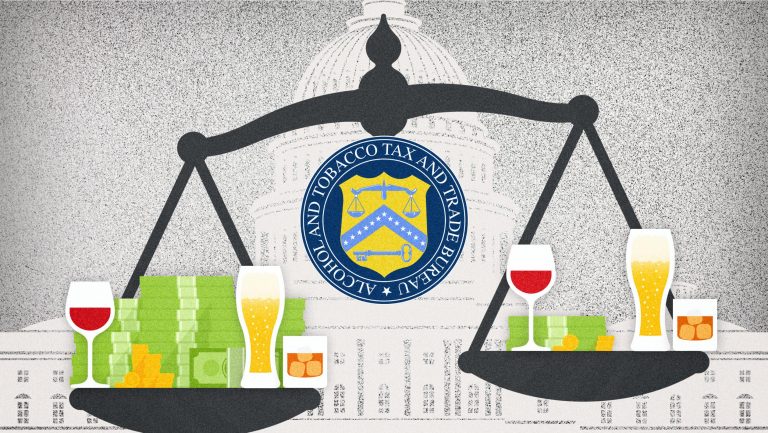

It’s an exciting year for Wigle Whiskey: The family-owned Pittsburgh distillery will get a $100,000 boost in 2018 thanks to new tax laws passed by the United States Congress at the end of 2017.

While the Republican-sponsored Tax Cut and Jobs Act is causing turbulence and prompting questions across the country, the drinks industry has been quietly celebrating its passage. Included in the tax overhaul is the Craft Beverage Modernization and Tax Reform Act—the first update to alcohol tax laws since 1991—which Congress’s nonpartisan Joint Committee on Taxation estimates will bring $4.2 billion in tax savings to the industry over two years.

“It’s monumental,” says Bob Pease, the president and CEO of the Brewers Association, which represents small and independent craft brewers. Mark Shilling, the president of the board of directors of the American Craft Spirits Association (ACSA), calls the new legislation “the biggest deal for the spirits production part of the industry since Prohibition.”

Don’t miss the latest drinks industry news and insights. Sign up for our award-winning newsletters and get insider intel, resources, and trends delivered to your inbox every week.

For Wigle Whiskey, “it’s game changing,” says Meredith Meyer Grelli, one of the distillery’s owners. With the expected tax savings, her eight-year-old business is hiring another distiller and a marketing production manager, bringing the number of full-time employees to 20. Plans also include the increase in production of their 30,000-proof-gallon distillery by 20 percent. “It’s a funny situation for us,” Grelli says, “because we’ve personally never been on the front lines of pushing for tax reductions. It’s not really a part of our personal politics, but I can tell you now, living through this, I can see the impact.”

The new legislation corresponds with the evolution of the drinks business—acknowledging the growth of small, local producers, the way in which alcohol is produced, and the variety of alcohol products consumers are drinking—by equalizing tax and regulation policy. And, as demonstrated by Wigle, the laws aim to add jobs, increase production, and be a source of significant reinvestment into beer, wine, and distilled spirits businesses.

Shilling, who cofounded Revolution Spirits and is now with Treaty Oak Brewing and Distilling in Austin, Texas, says that just weeks after the bill passed, ACSA members were reinvesting in their own businesses. “We’re surveying our folks,” he says, “and seeing that there’s going to be a considerable amount of new hiring—people are bringing on new employees either to expand their production or to expand their sales and marketing efforts. They’re buying new equipment. [Treaty Oak], in fact, is building a new tasting room and is going to be able to expand the aging for the aged spirits, and we’re going to be buying new barrels and putting more stock back.”

Key Provisions

Here are the main provisions of the new legislation that drinks businesses should be aware of.

Big Cuts for Craft Distillers

Small producers of distilled spirits will likely see some of the largest cuts. The new law reduces the federal excise tax 80 percent, from $13.50 to $2.70 per gallon, for the first 100,000 proof gallons removed from bond per year. The excise tax is reduced to $13.34 for proof gallons between 100,000 and 22,130,000, and it remains at $13.50 for amounts above 22,130,000. The new law will also allow spirits to be transferred in nonbulk containers (such as bottles) without paying a tax.

“As a relatively new part of the industry, compared to beer and wine, we are looking to be treated with equality in the regulatory system,” Shilling says. “This is the first big step toward that. It’s kind of like craft distilling grows up.”

Also included in the law is a provision making importers of distilled spirits eligible for the lower rates. However, there are concerns that this could become a loophole whereby larger foreign producers could take advantage of legislation meant to focus on “craft” producers. Adam Looney, a senior fellow at the Brookings Institute, wrote a report outlining his concern that it’s misleading to imagine that this law will mostly affect craft and smaller producers; he believes both larger U.S. producers and foreign-owned makers will see the most benefits.

Scott Rosenbaum, a spirits strategist for importer and distributor T. Edward Wines and Spirits and a contributing editor to SevenFifty Daily, sees it this way: “Technically, I could work with a giant producer,” he says, “but if I’m a small importer, that large producer benefits from the reduced tax rate. But to be fair, [the importer] still benefits. Any importer is going to be an American company. So [the legislation] is still going to benefit small businesses in that regard—but not necessarily small producers.”

Shilling dismisses criticism that the legislation could taint the term “craft,” which Looney’s piece suggests. The word doesn’t have a legal or regulatory definition. “It’s incumbent upon us as craft distillers to educate our customers and not necessarily hang the benefit on the use of the word,” he says.

Wine Credits Expanded

For wine, the new tax reform act provides savings to medium and large wineries, as well as to importers of foreign-produced wines, by extending the existing “small producer tax credit” to all wineries and not just those producing less than 250,000 gallons of domestic wine annually. “Proportionally, in the wine industry, there’s a sweet spot of producers who make 100,000 to 350,000 gallons of wine, and they’ll see the real benefits,” says Michael Kaiser, the vice president of public affairs for WineAmerica, a trade association representing U.S. wineries.

The new laws expand the definition of “table wine” by raising the alcohol by volume (ABV) requirement from a maximum of 14% to 16%—a reflection, Kaiser says, of the way American wines, particularly in California, are made. The change represents a 50-cents-per-gallon savings for wines between 14% and 16% ABV. Now, says Kaiser, “you won’t see people manipulating their wine to get lower alcohol content just so they can pay less tax.”

All still wines under 16% ABV will now be taxed at the existing rate of $1.07 per wine gallon, but wineries will receive annual tax credits of $1 per wine gallon for the first 30,000 gallons, 90 cents per wine gallon for the next 100,000 gallons, and 53.5 cents per wine gallon for the next 620,000 gallons. Production over 750,000 wine gallons will not receive a credit.

The new laws also make sparkling wine producers and importers eligible for the same tax credits for the first time.

Tax credit rules for hard cider have expanded to other fruits (not just apples) and increased cider’s allowable ABV, while other low-alcohol-by-volume beverages, such as mead and beverages made from grapes, are now eligible to be taxed at the lowest applicable rate for still wine. (Details of those rates can be found on the Alcohol and Tobacco Tax and Trade Bureau, or TTB, website.)

“There was a reason why all of a sudden the wine-cooler craze just ended, and that reason was because they had to pay the sparkling wine tax rate of $3.40 [per gallon],” Kaiser says.

Beer Benefits

The provisions of the Craft Beverage Modernization and Tax Reform Act cut the federal excise tax on beer in half, from $7 per barrel to $3.50 on the first 60,000 barrels, for domestic brewers producing 2 million barrels or less annually. The amount above 60,000 barrels is taxed at $16 a barrel. For large brewers and importers, the first 6 million barrels are taxed at $16 a barrel, an 11 percent savings, while anything higher remains at $18 a barrel.

“Breweries will take this savings … and reinvest [the money] into their businesses,” Pease says. For example, he notes, Left Hand Brewing in Longmont, Colorado, has already said that it will be hiring new salespeople. “The bill was never positioned by the Brewers Association [in such a way] that it would result in cheaper beer prices for the beer drinker,” says Pease. “It was to help small business owners grow their businesses.”

As with the provisions for distilled spirits, the new law doesn’t tax transfers between bonded facilities if certain requirements are met. This, Pease predicts, could spark more collaborations between small breweries.

Navigating the Legislation’s Limited Term

As it now stands, the law will expire in two years. While it’s not unique for provisions in the country’s tax code to sunset—meaning that they’ll automatically be terminated unless reauthorized by Congress—the most recent version of the stand-alone bill, sponsored by Senator Ron Wyden, D-OR, and introduced with bipartisan support, was meant to be permanent.

Grelli, of Wigle Whiskey, remains cautiously optimistic: “Like many small family businesses, we’re pretty conservative, and so we only hire when we know we can support [employees]. And we believe we’ll continue to grow … We also continue to see a nice overall industry growth. Even if this tax bill is short lived, the growth [will have] a longer curve to it.”

Rosenbaum, though, is more wary. “The issue is, will I hire someone with all this up in the air?” he says. “Everything is in a holding pattern. How can you make an informed decision and plan without knowing that these breaks are going to exist 24 months in the future? If they are, it’s a tremendous boon, but if they disappear, it’s [only] a little boost.”

Industry leaders, while they say they’re optimistic about reauthorization, advise businesses to take advantage of the savings for 2018 and 2019 and consult their professional tax attorneys with questions.

“We don’t want to see this go away at the end of two years,” Shilling says, “but even if it does, it’s a huge temporary savings, and it really lifts a lot of small distilleries out of the difficulty of current cash flow and [helps them] get to the next level of sustainability. Take advantage of it while you have it and don’t spend out further than the two years, based on your sales and expected savings, until you know for sure … But anything reinvested in businesses is going to put them on a better footing for 2020, regardless of reauthorization.”

Shilling and other representatives from industry associations say they are dedicated to making the Craft Beverage Modernization and Tax Reform Act permanent and that increased membership will help them in their efforts.

“We think we have a solid case on why this is sound public policy,” says Pease. “And over 23 months, it will demonstrate that reducing the rate on brewers is going to [contribute] significantly to the economy.”

Shilling details some of the benefits he sees from the new legislation: “The impact is not just on the distillery itself—it’s going to be more money going back to the community. As a small distillery grows, it will presumably pay more in local sales taxes, local property taxes, local payroll taxes, so it’s not like the savings of the excise tax money is not going anywhere. It’s actually helping improve local tax bases as well.”

Resources

Additional details and resources about the Craft Beverage Modernization and Tax Reform Act can be found at these sources: TTB, Tax Cut and Jobs Act, WineAmerica, Brewers Association, American Craft Spirits Association.

Dispatch

Sign up for our award-winning newsletter

Don’t miss the latest drinks industry news and insights—delivered to your inbox every week.

Alicia Cypress is following her passion for wine after spending more than 20 years as a journalist at National Public Radio and the Washington Post. She’s currently a managing editor at Reviewed.com, a part of the USA Today Network, and she writes a wine blog, itswinebyme.com. She’s received the WSET 2 certification (with distinction) and hopes to continue her studies. Talk about wine with her on Twitter or Instagram.